State of Pest, Lawn and Landscape M&A

In their careers, Greg Clendenin and Graham Anthony have closed over 100 transactions in the Pest Control, Lawn Spray and Landscape (“Green”) Industries. As The Clendenin Anthony Partnership, Graham and Greg successfully sold nine Green Industry Companies in 2025 as well as extensive discussions with buyers and sellers to discover the best pricing & terms available. As such, Clendenin-Anthony has a front row seat to understanding the range of pricing and multiples being received from buyers in M&A transactions today.

AS ANY GREEN INDUSTRY BUSINESS OWNER KNOWS, Private Equity (PE) has been actively courting Pest Control, Lawn Spray and Landscape Maintenance firms (“Green Companies”). What was formerly the domain of Strategic Industry buyers has become in fashion with the Private Equity community—driving demand and pricing.

While Pest Control businesses command increasingly high pricing, the past few years have also brought increased interest in (and increasing pricing to) Lawn Spray and Landscape Maintenance Companies as buyers seek businesses with similar economic profiles to Pest Control in other Green Industries.

Key Value Drivers

As Green Company owners prepare for a sale—whether for this year or several years from now—it is helpful to know what has made Green Industries attractive to both PE and Strategic buyers and what operational/economic profiles these buyers typically seek. We have identified seven categories buyers pay attention to when considering a purchase.

FOCUS: A firm’s degree of specialization. Buyers tend to seek ”pure-play” assets—firms that are largely focused on either a commercial or residential customer base and that provide predominantly one type of service, such as:

Commercial Landscape Maintenance

Residential Landscape Maintenance (particularly high-end)

Lawn Spray

Commercial Pest Control

Residential Pest Control

Aquatic Weed Control

This is what we are seeing right now. Bear in mind, however, that a buyer’s focus often changes over time as they grow and seek more firms to acquire, leading them to add services or customer bases they might not have considered a year earlier.

The key to a higher sale price is to know who is buying what when—and put your well-tailored offering in front of them at just the right time.

That said, there are very few true 100% pure-play Green Companies. Most have a mix of customers and services that cross the Commercial/Residential and Landscape/Lawn/Pest divides. We have observed that those that are primarily (say 80%+) one type of customer and (say 70%+) one type of service will receive a premium price compared with those that are more of a blend.

Are there blend buyers? Sure. It just affects which buyers will be most interested in and what level of competition can be created to drive price.

SIZE: A firm’s revenue. Bigger businesses are valued more highly than smaller ones, simply because the buyer can buy more revenue in one go. Green Businesses face valuation inflection points at different sizes:

Businesses under $1mm of revenue are more challenging to sell and tend to trade at lower multiples.

Businesses between $1mm and $5mm of revenue will typically be tucked in, and their valuation will be driven by their customer base and services’ degree of Focus (see above), their Route Economics (see below) and the Gross Margin (see below) they are earning on their customers.

Businesses between $5mm and $15mm of revenue garner strong multiples. These firms can be add-ons for a buyer wanting to enter a new market or an in-market add-on to bulk up a branch.

Businesses over $15mm of revenue are rarer and can often get “nosebleed” valuations. These firms are large enough to be platforms for small PE players. Their value will be driven in part by the quality of the Management Team (if it plans to stay) and their prowess in systematizing their business.

RECURRING REVENUE: Whether a service is provided on an ongoing basis versus a one-off. As Greg has said in his talks, “Recurring Revenue is the Eighth Wonder of the World.” Simply put, buyers place a much lower multiple (if any) on one-time work. Hence Termite Initial garners a much lower multiple than Quarterly General Pest Control (GPC). Most Landscape Install firms garner less buyer interest than Landscape Maintenance ones.

Preferences for types of recurring revenue change over time. In the late 1990s and early 2000s, Termite Renewals were valued far more highly than General Pest Control. Now they can be valued above or below GPC based on retention rates.

REVENUE RETENTION: Whether a business’s revenue is recurring and derives from a stable customer base. Firms with high retention rates (low customer churn) are viewed as better-managed firms and worth more money than firms with significant churn. Even a few percentage points of churn make a material difference in valuation.

ROUTE ECONOMICS: The amount of revenue per truck, less the cost of the technician, chemistry, gasoline and other vehicle expenses. How much Contribution Margin (profit toward overhead) does a given “Route” provide? Different buyers track different metrics, but in general, clearly presented profitable Route Economics will drive price: the higher the Contribution Margin from the Route, the more highly the buyers will value the business. For larger businesses, ditto the Branch Economics, the profitability of a given office, the Branch.

GROSS MARGIN: The delta between customer revenue and the hard costs of providing the service. A smaller firm’s customers being tucked into existing routes are to a large extent valued on the Gross Margin those customer accounts provide the new owner once layered on their existing routes.

EBITDA: Earnings Before Interest Taxes Depreciation and Amortization. A mouthful. In fact, Adjusted EBITDA is the base number on which most buyers apply an acquisition multiple to value a business. That amount is EBITDA PLUS the owner’s personal expenses that are not necessarily business-related as well as non-recurring business expenses, such as remodeling the office or installing a new air-conditioning system.

In truth, most buyers are (or should be) looking at free cash flow to them once they own the business. Depending on the size, smaller firms are more likely to be valued on Route Economics—or even Gross Margin on the service itself if the acquired customers are likely to be aggregated onto the buyer’s existing routes—adding Route density and increasing the profitability of each Route.

To summarize, a Green Business’s value is driven by the buyer pool: which buyers with which pricing preferences are competing for acquisitions based on a company’s:

Focus. Service type (e.g., Landscape, Lawn Spray, Pest Control), customer type (residential vs. commercial) and geographic region.

Size. A firm’s revenue.

Revenue stability. True recurring revenue and revenue retention (amount of churn)

Profitability. Route economics and gross margin (profit per customer)—and for larger firms, of the business overall.

Gross Margin: Customer revenue vs. the hard costs of providing the service.

Adjusted EBITDA: Earnings Before Interest Taxes Depreciation and Amortization plus the owner’s personal non-business expenses.

How Green Businesses present themselves to properly reflect these metrics will determine where in a given value range buyers will bid.

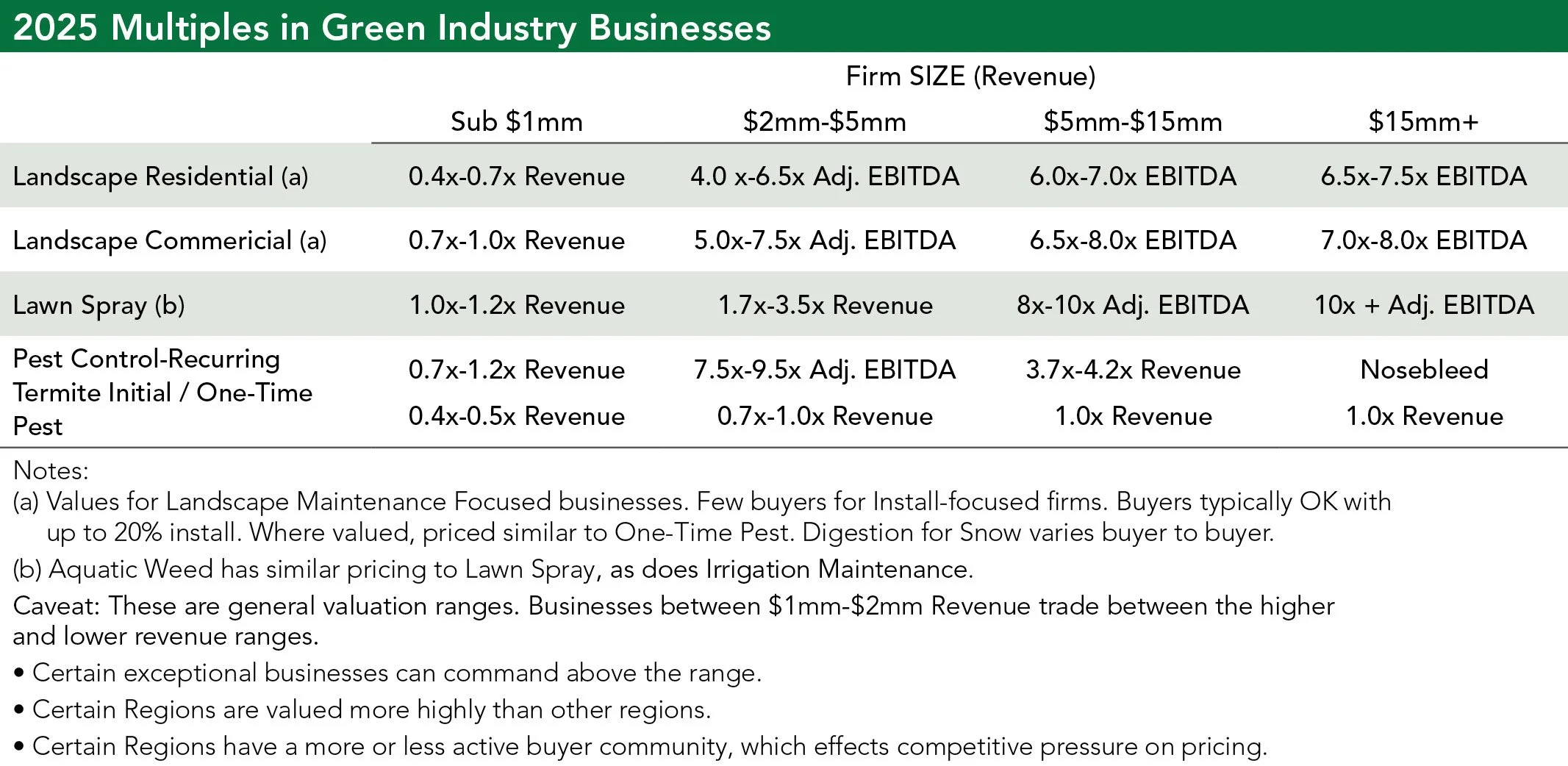

This table roughly depicts the ranges we saw for different types and sizes of Green Industry businesses in 2025. Bear in mind that these multiples are just representations of what we have seen in transactions during 2025. In the past we have seen both higher and lower multiples. We are seeing a strong start to 2026. Hopefully some 2026 transactions will exceed the multiples in this chart.

While the future may reflect the past, the only thing that truly establishes value is the price to which a willing buyer and a willing seller can come to terms.

Packaging the business correctly and presenting it to the right universe of buyers in the right way will maximize value. An advisor with a history of selling businesses to many different Strategic and Private Equity buyers are most likely to know which companies’ criteria are a close fit to the selling firm to ensure your company is matched up with the right buyers.

At Clendenin Anthony, we provide pre-sale planning and packaging, bring multiple buyers to the table, and negotiate the best deal for the owners of the Green Businesses we have been asked to help sell, shepherding the transaction through to closing. Because we have negotiated with dozens of specific buyers, often multiple times, in the past, we have a good sense of what each buyer is looking for, what they are trying to avoid and what they are willing to pay. We also know who is likely to be a good steward of the business and its customers and employees post-closing.

By presenting the business in a clear and concise manner tailored to fit within each buyer’s current plan and focus, and by running a straightforward and well managed sale process with multiple buyers, we are able to deliver the strongest valuations and successful transactions that meet our sell-side clients’ needs and preserve their hard-earned legacy.

For more information or a confidential conversation, contact Graham Anthony, ganthony@aadvisors.com (434) 989-5800 or Greg Clendenin gc@clendenincg.com (407) 948-0897.